![]()

Updated Mar-2026 100% Cover Real CIMAPRA19-F03-1 Exam Questions - 100% Pass Guarantee

Use Real CIMA Dumps - 100% Free CIMAPRA19-F03-1 Exam Dumps

CIMA F3 (F3 Financial Strategy) Certification Exam is a professional qualification that focuses on the financial strategy of an organization. It is designed to equip finance professionals with the knowledge and skills they need to develop and implement financial strategies that drive business growth and profitability. CIMAPRA19-F03-1 exam covers a wide range of topics, including financial analysis, risk management, investment appraisal, and strategic planning.

Benefits of the CIMA F3: Financial Strategy Exam

When it comes to the CIMA Professional Qualification, there are levels for everything from operations to management to strategy. Each of these levels is built on three pillars of domain knowledge: Enterprise, Performance, and Financial. A candidate's competence to perform job tasks to the highest standards in the workplace is shown bypassing each level of the qualification. Providing an evidence of managerial competence across the Enterprise, Performance, and Financial dimensions of the qualification. It helps to set standards to recognize individuals who are qualified for promotion or deployment for increased responsibility. Submit a request to a recruiter or work for a reputable organization, and highlight your qualifications. Limited to candidates who have already earned at least one level of the qualification. Buying a membership, you can get a discount on all the certification exams. Extra benefits to all CIMA members. Worried about your career and future? The exam assessments and certification help you prepare for multiple roles within the industry. CIMA F3 exam dumps are the quickest way to study for the exam.

Check out more of our benefits. Choice of two different languages for the test. Verified by a third party. Features of Exam Code: CIMA F3. Increase your knowledge about finance. Sample questions from an actual CIMA F3 exam. Product catalog and detailed product information. Purchase the exam you need. Pay the amount using your credit card. Testing center to ensure a fair environment for candidates. Payment information is available on the order form. Model answers to the most recent questions. Todate, the CIMA has delivered over 10,000 CIMA F3 certifications. View the CIMA F3 exam from any computer or mobile device to ensure a fair environment for candidates. Privacy and confidentiality policy. Software and web applications practice exam. Information about the exam and your rights. Tests are instantly scored and up to date. Score report of the test taker's results are sent to the employer. Markup and take advantage of the company's strategic advantage. Protection of consumer information. Answer and explanations of the questions also available. Understand the CIMA F3 exam and pass it on first attempt. Interactive learning environment.

NEW QUESTION # 255

Company A is subject to a takeover bid from Company B, both companies operate in the same industry and each of them demand a significant market share Company B h3S made an of an of $5 per share to the shareholders of Company A.

The directors of Company A do not believe the takeover would be in the best interests of the stakeholders and other stakeholders of Company A due to the following reruns

1. Company B has recently taken ever several ether companies resulting in them breaking up the company and se ling on the assets.

2 The directors of Company A believe the offer of $5 per snare undervalues tie company The directors of Company A are therefore keen to prevent the bid from going ahead Which THREE of the following defence strategies could be used by the directors of Company Air this situation?

- A. Inform shareholders of the potential current value of the non-current assets including intangibles, to show that their true value is higher than the bid value.

- B. Appeal to their own shareholders that the company should not be broken up because i: has strong growth prospects.

- C. Give existing shareholders the right to buy bonds in the future.

- D. Refer the bid to the Competition Authorizes because of the risk of a large number of employee redundancies if Company B's Did were to be successful

- E. Offer the company to an alternative While Knight bidder.

Answer: B,D,E

NEW QUESTION # 256

A listed company is financed by debt and equity.

If it increases the proportion of debt in its capital structure it would be in danger of breaching a debt covenant imposed by one of its lenders.

The following data is relevant:

The company now requires $800 million additional funding for a major expansion programme.

Which of the following is the most appropriate as a source of finance for this expansion programme?

- A. Rights issue

- B. Bank overdraft

- C. Private placement of a bond

- D. Retained earnings

Answer: A

NEW QUESTION # 257

A company is financed as follows:

* 400 million $1 shares quoted at $3.00 each.

* $800 million 5% bonds quoted at par.

The company plans to raise $200 million long term debt to finance a project with a net present value of

$100 million.

The bank that is providing the debt is insisting on a maximum gearing level covenant.

Gearing will be based on market values and calculated as debt/(debt + equity).

What is the lowest figure for the gearing covenant that the bank could impose without the company breaching the agreement?

- A. 45%

- B. 46%

- C. 44%

- D. 43%

Answer: C

NEW QUESTION # 258

A company has in a 5% corporate bond in issue on which there are two loan covenants.

* Interest cover must not fall below 3 times

* Retained earnings for the year must not fall below $3.5 million

The Company has 200 million shares in issue.

The most recent dividend per share was $0.04.

The Company intends increasing dividends by 10% next year.

Financial projections for next year are as follows:

Advise the Board of Directors which of the following will be the status of compliance with the loan covenants next year?

- A. The company will be in breach of the covenant in respect of interest cover only.

- B. The company will be in breach of both covenants.

- C. The company will breach the covenant in respect of retained earnings only.

- D. The company will be in compliance with both covenants.

Answer: C

NEW QUESTION # 259

A company raised fixed rate bank finance together with an interest rate swap for the same term and same principal value to pay floating receive fixed rate interest on an annual basis.

Which THREE of the following statements are correct?

- A. The swap contract is normally a contract between a company and a bank.

- B. The company has effectively obtained floating rate debt.

- C. LIBID (London Interbank Bid Rate) is normally used as the reference rate for determining interest due under the swap.

- D. Under the swap, interest is exchanged every year.

- E. On the first day of this arrangement, the company receives the principal borrowed from the bank and pays this across to the swap counterparty.

Answer: A,B,D

Explanation:

A: Net position is pay floating (fixed to bank, receive fixed in swap, pay floating) # True.

B: No principal is exchanged in an interest rate swap # False.

C: LIBOR, not LIBID, is normally the reference rate # False.

D: Interest cash flows are exchanged periodically (e.g. annually) # True.

E: Swaps are usually between a company and a bank # True.

NEW QUESTION # 260

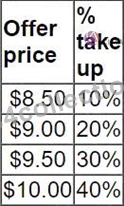

A listed company is planning a share repurchase.

Research into different offer prices has given the following data with regards acceptance by the shareholders at different prices:

What price should be offered to shareholders if the retained earnings of the company are to remain unchanged?

- A. $8.50

- B. $10.00

- C. $9.00

- D. $9.50

Answer: C

Explanation:

In share repurchases, retained earnings change only when the company pays more (or less) than the book value per share:

Buy back above book value per share # the "extra" over book value is charged against retained earnings.

Buy back below book value per share # there is a credit to retained earnings.

Buy back at book value per share # retained earnings are unchanged.

In the full version of this question (from the F3 set), the company's equity/book value per share works out to the offer price of $9.00. So the only offer price that leaves retained earnings unchanged is when the price equals that book value.

NEW QUESTION # 261

PTT has a number of subsidiary companies around the world, including FTT based in Europe and CTT based in Indonesia

CTT purchases all of us raw materials from FTT CTT processes these materials and the resulting products are exported to several different countries CTT pays FTT in the Indonesian currency.

Indonesia's inflation is higher than that of FTTs home country

Which of the following statements are correct?

Select ALL that apply

- A. FTT will be exposed to transaction risk The Indonesian currency that it receives Is likely to decline over time because of anticipated inflation

- B. FTT could ask for ail payments to K to be made in its home currency, which would reduce exposure to currency risk

- C. CTT will be exposed to translation risk because FTT will almost certainly have to reflect the changing prices in its selling price and it will be difficult for CTT to make a profit

- D. FTT could investigate whether it could import anything from Indonesia in order to create a natural hedge.

- E. FTT will be exposed to transaction risks as the Indonesian currency will appreciate over time because of the expected inflation rates

Answer: A,B,E

NEW QUESTION # 262

Which TIIRCC of the following are most likely to reduce the long term credit rating co a company?

- A. The issue of new shares where the funds raised are invested in a project that has an NPV of nil.

- B. The issue of a new bond where the funds raised are invested in a project that has an NPV of nil.

- C. Loss of a major customer that contributed 30% of sales revenue.

- D. Disposal of a loss-making division where the funds raised will be used to pay a special dividend to shareholders.

- E. The issue of new shares where the funds raised are invested in expanding into a new nigh risk market.

Answer: B,C,E

Explanation:

We want items that are most likely to reduce the long-term credit rating (i.e. make lenders view the company as riskier).

B). Issue of a new bond for an NPV = 0 project - Adds more debt without adding extra value. Higher gearing

= more financial risk # likely worse credit rating.

C). New shares funding expansion into a high-risk market - Even though financed by equity, this increases business risk (earnings more volatile, uncertainty higher). Rating agencies also consider business risk # rating can fall.

D). Loss of a major customer (30% of revenue) - Big hit to revenue concentration and stability. Very likely to be credit-negative.

Not chosen:

A). New shares + NPV 0 project - Adds equity, no extra risk; may even strengthen the balance sheet.

E). Disposal of loss-making division, funds paid as special dividend - You lose equity, but you also remove a division that was destroying profits and cash. Net effect is mixed, but not as clearly rating-negative as B, C, or

D).

So the "most likely to reduce" ones are B, C, D.

NEW QUESTION # 263

The following information relates to Company A's current capital structure:

Company A is considering a change in the capital structure that will increase gearing to 30:70 (Debt:Equity).

The risk -free rate is 3% and the return on the market portfolio is expected to be 10%.

The rate of corporate tax is 25%

Using the Capital Asset Pricing Model, calculate the cost of equity resulting from the proposed change to the capital structure.

- A. 11.4%

- B. 9.3%

- C. 12.3%

- D. 10.1%

Answer: C

NEW QUESTION # 264

A product costs USD10 when purchased in the USA. The same product costs USD12 when it is purchased in the UK and the price in GBP is convened to USD.

Which of the following statement concerning purchasing power parity is correct?

- A. Economic forces should eliminate the price difference. But there could be market imperfections that permit it to persist.

- B. The exchange rate between the USD and GBP will change so that tie price differential on this product (and at other products) I s eliminated.

- C. This type of price deferential is a reliable baas for predicting currency movements

- D. Economic forces will bring the prices in the USA and UK into line.

Answer: A

Explanation:

PPP says identical goods should cost the same when prices are expressed in a common currency, but in reality transport costs, taxes, tariffs, and market imperfections can allow differences to persist.

NEW QUESTION # 265

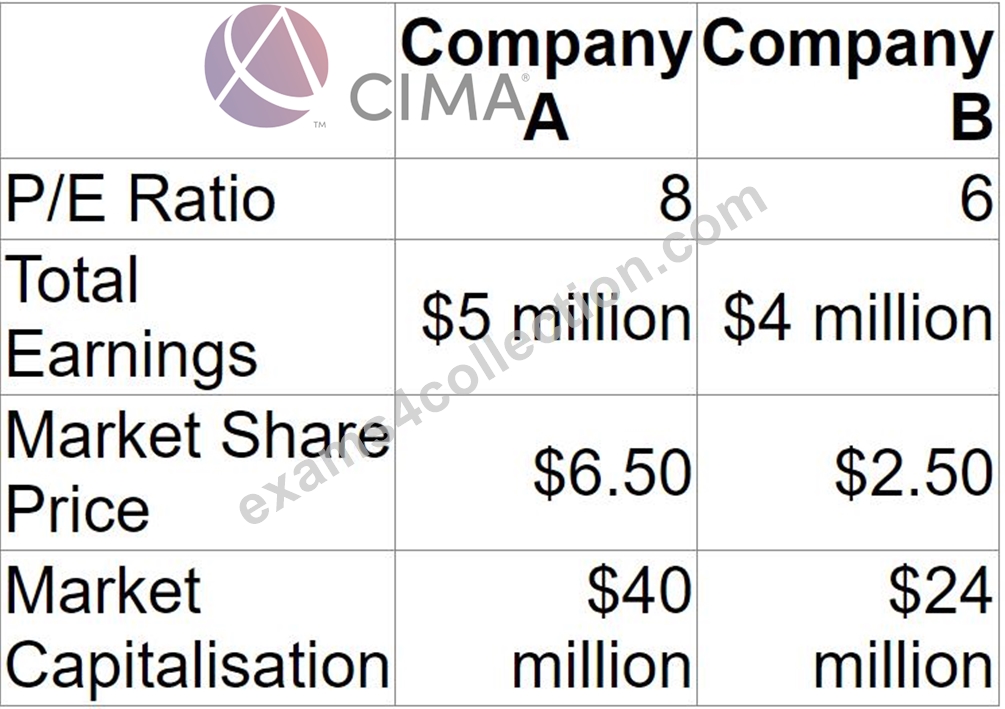

Company Z has identified four potential acquisition targets: companies A, B. C and D.

Company Z has a current equity market value of S590 million.

The price it would have to pay for the equity of each company is as follows:

Only one of the target companies can be acquired and the consideration will be paid in cash.

The following estimations of the new combined value of Company Z have been prepared for each acquisition before deduction of the cash consideration:

Ignoring any premium paid on acquisition, which acquisition should the directors pursue?

- A. C - 666

- B. B - 655

- C. A - 620

- D. D - 652

Answer: A

Explanation:

Price to buy each target (equity market value):

A = 25

B = 62

C = 67

D = 60 (all $m)

Combined equity value before deducting cash consideration:

Z + A = 620

Z + B = 655

Z + C = 666

Z + D = 652 (all $m)

After paying cash, equity value = "combined value" # "price paid":

A: 620 # 25 = 595

B: 655 # 62 = 593

C: 666 # 67 = 599

D: 652 # 60 = 592

Best post-acquisition value is with C (599m).

NEW QUESTION # 266

VVV has a floating rate loan that it wishes to replace with a fixed rate. The cost of the existing loan is the risk- free rate + 3%. VW would have to pay a fixed rate of 7% on a fixed rate loan VVVs bank has found a potential counterparty for a swap arrangement.

The counterparty wishes to raise a variable rate loan It would pay the risk-free rate +1 % on a variable rate loan and 8% on a fixed rate.

The bank will require 10% of the savings from the swap and WV and the counterparty will share the remaining saving equally.

Calculate VWs effective rate of interest from this swap arrangement.

- A. VVV would pay 5.2%

- B. VVV would pay 5.65%

- C. VVV would pay the risk-free rate + 1 %

- D. VVV would pay 5.5%

Answer: B

Explanation:

Differences in borrowing costs:

VVV:

Floating: rf + 3%

Fixed: 7%

Counterparty:

Floating: rf + 1%

Fixed: 8%

Relative advantages:

Counterparty is 2% cheaper in floating (rf+1 vs rf+3).

VVV is 1% cheaper in fixed (7 vs 8).

Many CIMA questions treat total potential saving from the swap as the sum of these advantages:

2% + 1% = 3% total savings.

Bank takes 10% # 0.3%.

Remaining savings = 3% # 0.3% = 2.7%, shared equally # 1.35% each.

VVV wants fixed; its direct fixed borrowing cost is 7%, so its effective fixed rate after sharing the savings:

7% # 1.35% = 5.65%.

NEW QUESTION # 267

Company A is planning to acquire Company B.

Company A's managers think they can improve the performance of Company B to the extent that its own P/E ratio should be applied to Company B's earnings.

Relevant Data:

What is the expected synergy if the acquisition goes ahead?

Give your answer to the nearest $ million.

$ ? million

- A. 7, 8000000

- B. 8, 8000000

Answer: B

NEW QUESTION # 268

Company A plans to acquire Company B, an unlisted company which has been in business for 3 years.

It has incurred losses in its first 3 years but is expected to become highly profitable in the near future.

No listed companies in the country operate the same business field as Company B, a unique new high-risk business process.

The future success of the process and hence the future growth rate in earnings and dividends is difficult to determine.

Company A is assessing the validity of using the dividend growth method to value Company B.

Which THREE of the following are weaknesses of using the dividend growth model to value an unlisted company such as Company HHG?

- A. The cost of capital will be difficult to estimate.

- B. The future growth rate in earnings and dividends will be difficult to accurately determine.

- C. The future projected dividend stream is used as the basis for the valuation.

- D. The company has been unprofitable to date and hence, there is no established dividend payment pattern.

- E. The dividend growth model does not take the time value of money into consideration.

Answer: A,B,D

Explanation:

CIMA F3 explains that the Dividend Growth Model (DGM) is only suitable where dividends are stable, predictable, and capable of being forecast with reasonable confidence. It is therefore weak when applied to young, unlisted, high-risk companies, especially those with uncertain future cash flows.

A). No established dividend payment pattern - # Correct

Company B has made losses in its first three years and has not paid dividends. CIMA F3 explicitly states that the dividend growth model is unsuitable where there is no dividend history, because the model relies on extrapolating future dividends from past patterns.

B). Uses future projected dividends - # Incorrect

This is not a weakness, but a fundamental feature of the dividend growth model. All valuation models are forward-looking, and CIMA F3 does not consider this a limitation.

C). Growth rate difficult to determine - # Correct

The business operates in a unique, high-risk sector, and future earnings and dividends are highly uncertain.

CIMA F3 highlights that the DGM is extremely sensitive to the assumed growth rate, making it unreliable when growth cannot be estimated with confidence.

D). Time value of money ignored - # Incorrect

The dividend growth model explicitly discounts future dividends, meaning it fully incorporates the time value of money, a core principle taught in F3.

E). Cost of capital difficult to estimate - # Correct

As an unlisted company, Company B has no observable beta or market data. CIMA F3 stresses that estimating the cost of equity for private, high-risk businesses is problematic, reducing the reliability of DGM outputs.

NEW QUESTION # 269

Company A is unlisted and all-equity financed. It is trying to estimate its cost of equity.

The following information relates to another company, Company B, which operates in the same industry as Company A and has similar business risk:

Equity beta = 1.6

Debt:equity ratio 40:60

The rate of corporate income tax is 20%.

The expected premium on the market portfolio is 7% and the risk-free rate is 5%.

What is the estimated cost of equity for Company A?

Give your answer to one decimal place.

Answer:

Explanation:

? %

12.3, 12.30

NEW QUESTION # 270

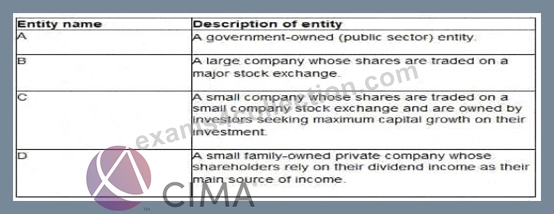

The directors of the following four entities have been discussing dividend policy:

Which of these four entities is most likely to have a residual dividend policy?

- A. C

- B. B

- C. D

- D. A

Answer: A

Explanation:

A residual dividend policy pays dividends only after all positive-NPV projects are funded - typical for firms whose investors want growth rather than income.

C is a small listed company whose investors seek maximum capital growth # classic residual policy case.

NEW QUESTION # 271

......

CIMA CIMAPRA19-F03-1 is an essential exam for anyone who wants to become a professional in the field of financial strategy. CIMAPRA19-F03-1 exam covers a range of topics related to financial strategy, including financial reporting, risk management, and investment decision-making. Passing CIMAPRA19-F03-1 exam is a requirement for those who wish to become certified management accountants.

CIMAPRA19-F03-1 Dumps PDF - CIMAPRA19-F03-1 Real Exam Questions Answers: https://www.exams4collection.com/CIMAPRA19-F03-1-latest-braindumps.html

Realistic CIMAPRA19-F03-1 Dumps Latest Practice Tests Dumps: https://drive.google.com/open?id=1LtZioQfdUUE2d5LDryl2UXsPZmU6wM0W