![]()

Verified ClaimCenter-Business-Analysts dumps Q&As 100% Pass in First Attempt Guaranteed Updated Dump from Exams4Collection

Pass Guidewire Certified Professional ClaimCenter-Business-Analysts Exam With 52 Questions

Guidewire ClaimCenter-Business-Analysts Exam Syllabus Topics:

| Topic | Details |

|---|---|

| Topic 1 |

|

| Topic 2 |

|

| Topic 3 |

|

| Topic 4 |

|

NEW QUESTION # 25

Succeed Insurance is implementing a slightly modified version of ClaimCenter to suit its organization's needs.

The modification will include adding two new required fields to the standard user interface to capture the reporter's Preferred Language and Preferred Contact Time. This requirement is critical for Succeed to improve efficiency and the expediency of claims processing in its region.

Under which ClaimCenter theme will the User Story Card be found for documenting these requirements?

- A. Settle/Close

- B. Intake

- C. Adjudicate

- D. Special Services

Answer: B

Explanation:

In the Guidewire implementation methodology, User Stories are categorized into Themes that align with the high-level business processes of the claim lifecycle.

* Intake (Option A):TheIntaketheme covers theFirst Notice of Loss (FNOL)process and the "New Claim Wizard." The requirement specified is to capture data regarding the "Reporter" (the person reporting the loss) and their contact preferences. In ClaimCenter, Reporter information is collected at the very beginning of the New Claim Wizard (Step 1: Search/Create Policy and Reporter). Because this data entry occurs during the initial setup of the claim, the User Story governing these UI changes belongs to theIntaketheme.

* Context:Improving "expediency of claims processing" often relies on accurate data capture at the Intake stage so that downstream assignment and communication can be handled correctly from the start.

Why other options are incorrect:

* Adjudicate (B):This theme covers the investigation, evaluation, and negotiation phases that occurafter the claim is created.

* Settle/Close (D):This theme covers the payment issuance and final closure of the file.

* Special Services (C):This typically refers to Vendor Management or specialized sub-processes, not the core FNOL reporter data.

NEW QUESTION # 26

A claim for an auto accident in California has been assigned to an insurance Adjuster in the Midwest region for investigation and processing. The claim has been flagged as "Low Complexity" in ClaimCenter. The Adjuster has an authority limit for total reserves of $30,000 and has created reserves totaling $35,000.

What is the correct approval routing for this transaction?

- A. The transaction will require approval from another team member who has the authority limit to approve.

- B. The transaction will require approval from the Supervisor of the group.

- C. This transaction will not require approval because the claim is identified as low complexity.

- D. This transaction will require approval because the Adjuster does not work in the same region where the claim was reported.

Answer: B

Explanation:

Based on theGuidewire ClaimCenter Financials and Authority Limitsdocumentation, the correct behavior for this scenario is determined by the strict enforcement ofAuthority Limits, regardless of claim complexity or geographic region.

In ClaimCenter, every user is assigned specific authority limits for various financial transactions, including reserves, payments, and recovery reserves. These limits are absolute constraints designed to control financial exposure. In the scenario provided, the Adjuster attempted to set a reserve of$35,000, which exceeds their authorized limit of$30,000.

When a user submits a financial transaction that exceeds their pre-configured authority limit, ClaimCenter automatically triggers anApproval Workflow. The system validates the transaction amount against the user's limit at the time of submission. Since the limit is breached, the transaction is not committed immediately to the database as "Submitted"; instead, it enters a"Pending Approval"status.

Routing Logic:

The standard, out-of-the-box approval routing logic in ClaimCenter follows the Group Hierarchy.

* The system identifies the group to which the Adjuster belongs.

* It creates anApproval Activity.

* This activity is assigned to theSupervisorof that group.

The Supervisor must then review the transaction. If the Supervisor has sufficient authority (greater than

$35,000), they can approve it. If the Supervisor also lacks sufficient authority, they must still "approve" it to escalate the request further up the hierarchy totheirmanager, until it reaches a user with sufficient limits.

Why other options are incorrect:

* A (Complexity):Claim complexity flags (e.g., "Low Complexity") are often used forAssignmentrules (Segment-based assignment) or straight-through processing ofdocuments, but they do not override Financial Authoritycontrols. A low-complexity claim still requires financial oversight if the dollar amount is high.

* B (Peer Approval):Approval routing is hierarchical, not peer-to-peer. It does not look for "any" team member; it looks specifically for the defined Supervisor.

* C (Region):The region mismatch might trigger an assignment rule or a validation warning depending on configuration, but the specific trigger for theapprovalhere is purely the financial discrepancy ($35k

> $30k), not the geography.

NEW QUESTION # 27

Satisfied with the outcome of a Requirements Workshop, a Business Analyst (BA) attributed the success to preparation. The assigned task had been to document the requirements for capturing details on vehicle incidents for Personal Auto.

* Before the session, the BA reviewed ClaimCenter functionality by creating a new Personal Auto Claim involving physical damage to a vehicle.

* During review, the BA saw that ClaimCenter did not have a graphical representation of a vehicle with clickable hot spots to identify the damage areas like they have in their current application.

* Upon further research, the BA found that Guidewire does offer this functionality and even provides a Graphical Incident Capture Accelerator to ease implementation.

* During the workshop, the BA was able to clearly present all options for capturing vehicle incident details. Instead of having to develop the Vehicle Incident Capture functionality from scratch, the team was able to make a quick decision to add this functionality and end the meeting 30 minutes early.

Which two outcomes demonstrate the importance of preparing for a Requirements Workshop by becoming familiar with the features and functionality of ClaimCenter? (Choose two.)

- A. The BA was able to make decisions in advance about where gaps existed and where changes were needed.

- B. The BA was able to gain team acceptance of the base product process instead of the legacy system process.

- C. The BA prevented the team from rebuilding something in a less effective way.

- D. The BA was able to compare their legacy process to how ClaimCenter handles the same business process.

Answer: C,D

Explanation:

This scenario highlights the value of Feature Knowledge and Gap Analysis during preparation.

* Prevention of unnecessary work (Option A):Because the BA researched and found the "Graphical Incident Capture Accelerator," the team avoided the costly mistake of deciding to "develop the...

functionality from scratch." This is a direct outcome of the BA's preparation preventing an inefficient custom build.

* Comparison of Legacy vs. New (Option B):The text details that the BA "reviewed ClaimCenter functionality" and explicitly noted the difference ("saw that ClaimCenter did not have... like they have in their current application"). This ability to articulate the gap between theAs-Is(Legacy) and theTo-Be (Base ClaimCenter) allowed the BA to present the Accelerator as the perfect bridge solution.

Why other options are incorrect:

* Option C:The team didnotaccept the "base product process" (which lacked the graphics); they accepted theAccelerator(an add-on) to match the legacy expectation of clickable hot spots.

* Option D:The decision was not made "in advance." The text states the team made the "quick decision" during the workshop. The preparation enabled theteam'sdecision, but the BA did not make it unilaterally beforehand.

NEW QUESTION # 28

Succeed Insurance had an embarrassing event last month that had potential legal ramifications. One of their Customer Service Representatives (CSR) shared details of a celebrity's personal auto claim on social media.

Fortunately for Succeed, the celebrity decided not to pursue legal actions as long as Succeed agreed to resolve the potential for future occurrences within the next 30 days.

Succeed executives immediately reacted to the situation by establishing new guidelines regarding claim security. The Business Analyst (BA) assigned to the project researched ClaimCenter base product capabilities and held several requirements gathering sessions designed to document their strategy. The new requirements indicate that only authorized users should be looking at celebrity claims.

Which two features should be used to meet the new requirements? (Choose two.)

- A. Create an access profile for each claim security level

- B. Create a rule that tracks who has viewed secure claims

- C. Hide secure claim information fields

- D. Assign authority profiles to authorized users

- E. Specify the claim security types

Answer: A,E

Explanation:

To restrict access to sensitive claims (such as those involving celebrities) so that "only authorized users" can view them, a Business Analyst must utilize the Claim Security features in Guidewire.

* Specify Claim Security Types (Option A):The first step is to define the classification of the claim.

The system uses the ClaimSecurityType typelist. The BA would add a new typekey (e.g., "Celebrity" or

"High Profile") or use an existing one (e.g., "Sensitive") to flag these specific claims.

* Create/Assign Access Profiles (Option E):Access control in Guidewire is managed throughAccess Profiles(sometimes referred to within Role configurations). An Access Profile maps specificSecurity Levels(like the "Celebrity" type defined above) to permissions. To meet the requirement, the BA defines an Access Profile that grants "View" permission for the "Celebrity" security type and assigns this profileonlyto the authorized users (or roles). Users without this specific Access Profile will be unable to search for or view the claim.

Why other options are incorrect:

* Authority Profiles (B):In Guidewire terminology, "Authority" refers strictly toFinancial Authority (limits on reserves and payments), not data access visibility.

* Hide secure fields (C):This refers toField Level Security(masking specific data like a Tax ID). The requirement is to restrict access to theentire claim, not just specific fields.

* Tracking rules (D):While "Claim Access Auditing" (tracking history) is often enabled for sensitive claims, it is a detective control, not a preventive one. The requirement specifies that unauthorized users should not be looking at the claim at all, which requires the Access Profiles (preventive control).

NEW QUESTION # 29

Succeed Insurance requires that all vehicles involved in collisions be evaluated to determine if the vehicle is a total loss. A vehicle claim is deemed a total loss using a calculation based on points earned for selecting specific vehicle information.

What are two examples of acceptance criteria for this business requirement? (Choose two.)

- A. Validate the assignment to the Salvage Group when calculated points are 25 or greater.

- B. Add a question to the Total Loss Calculator that identifies the relevant damage.

- C. Ensure that the business rule generates the Review for Salvage Activity.

- D. Create a business rule to calculate total loss points.

Answer: A,C

Explanation:

Acceptance Criteria (AC) are specific conditions that the software must satisfy to be accepted by the user. In the context of a User Story, AC must be written as testable outcomes or verification steps (pass/fail conditions), not as implementation tasks for the developer.

* Option D (Testable Outcome):"Validate the assignment to the Salvage Group when calculated points are 25 or greater."This is a perfect example of AC. It describes a specific scenario (Points >= 25) and the expected system behavior (Assign to Salvage Group). A tester can run this scenario and objectively determine if the system passes or fails.

* Option A (Testable Outcome):"Ensure that the business rule generates the Review for Salvage Activity."Similarly, this describes the expectedresultof the logic. It does not tell the developerhowto write the code, but it tells the QA team what to look for (the creation of a specific Activity) to confirm the requirement is met.

Why other options are incorrect:

* Option B ("Add a question..."):This is anImplementation Task. It describes work the developer must do ("Add a question"), but it is not a criterion for verifying the end-to-end business value.

* Option C ("Create a business rule..."):This is also anImplementation Task. A user cannot "test" that a rule was created; they test theeffectof that rule (which is described in A and D). Acceptance criteria focus on the "What" (behavior), while tasks focus on the "How" (configuration).

Here are the 100% verified answers for Question 16 and Question 17, formatted as requested.

NEW QUESTION # 30

To help manage new user setup, Succeed Insurance would like all manager-level employees to be able to add new users to ClaimCenter. Some managers are already assigned the Community Admin role, which has a set of permissions for the administration of the ClaimCenter community model that includes the permission to create new users.

Where are two places the Business Analyst (BA) can go to view the permissions assigned to manager-level users? (Choose two.)

- A. Go to c:\GW10\ClaimCenter\build\dictionary\security\index.html to view the Security Dictionary

- B. Go to the Administration menu > Users & Security > Roles

- C. Go to c:\GW10\ClaimCenter\build\dictionary\data\index.html to view the Data Dictionary

- D. Go to the Administration menu > Users & Security > Authority Limits

- E. Go to the Administration menu > Users & Security > Users

Answer: A,B

Explanation:

To view the detailed System Permissions (such as usercreate, claimview, etc.) associated with a specific user role (like "Manager" or "Community Admin"), a Business Analyst has two primary methods: one within the application UI and one via generated documentation.

* Administration Menu > Users & Security > Roles (Option E):This is the direct User Interface method. By navigating to theRolespage in the Administration tab, the BA can select a specific role (e.

g., "Manager"). The detailed view of that role lists every system permission currently granted to it. This allows the BA to verify if the "usercreate" permission is present.

* Security Dictionary (Option B):For a comprehensive, searchable, and offline reference, the BA can access theSecurity Dictionary. This is a set of HTML files generated from the application's configuration (found in the build directory). It provides a complete matrix of all Roles, the Permissions assigned to them, and the Access Profiles configured in the system.

Why other options are incorrect:

* Data Dictionary (A):This documents theData Model(Entities and Typelists), not the security configuration.

* Users (C):While this screen lists users and their assigned roles, it does not display thedefinitions(the specific list of permissions) of those roles.

* Authority Limits (D):This screen managesFinanciallimits (dollar amounts for reserves/payments), not system access permissions.

NEW QUESTION # 31

Succeed Insurance handles a small volume of asbestos claims in their legacy system. These claims can remain open for many years to cover medical costs to claimants due to illnesses caused by exposure to asbestos in the workplace.

Succeed has the following requirements for paying these claims with the New Check Wizard:

. No indemnity (claim cost) payments can be made until a medical assessment of the claimant is completed.

. Expense payments can be made to cover Succeed's costs to process the claim.

Which feature in the base product can be extended to support both of these requirements?

- A. Authority Limits

- B. Financial holds

- C. Claim Maturity Level - Ability to pay

- D. Transaction approval rules

Answer: C

Explanation:

250 to 350 words From Exact Extract of Guidewire ClaimCenter Business Analyst documentation:

The requirement to block specific types of payments (Indemnity) while allowing others (Expenses) based on the status of claim data (Medical Assessment) is best handled by Validation Rules at the Ability to Pay level.

* Ability to Pay (Option D):In Guidewire ClaimCenter, the "Ability to Pay" is a specificValidation Level. When a user attempts to issue a check, the system runs a set of validation rules to ensure the claim has reached a sufficient level of maturity and data completeness. This is the "gatekeeper" for payments.

* How it works for this scenario:A Business Analyst can define a validation rule at the "Ability to Pay" level that states:"If the Payment Type is Indemnity AND the Medical Assessment is incomplete, then raise an error."

* Why it fits:This logic perfectly satisfies both requirements.

* It blocks Indemnity payments if the assessment is missing.

* It implicitly allows Expense payments to proceed because the rule only checks for Indemnity payments.

Why other options are incorrect:

* Authority Limits (A)control theamountof money a user can approve, not the prerequisites for payment.

* Transaction Approval Rules (B)are used to route checks for supervisory review based on criteria, not to block them entirely due to missing data.

* Financial Holds (C)are generally applied to a whole claim or exposure to suspendallpayments (or broadly all payments of a certain category). While possible to configure, they are less flexible than Validation Rules for checking specific data fields like "Medical Assessment" dynamically during the check wizard process.

NEW QUESTION # 32

Drivers for Rideshare companies need insurance that provides protection when they are driving the vehicle for personal reasons. This will be the Succeed Insurance standard Personal Auto Policy. However, they also need insurance to protect them from the increased risks associated with working as a Rideshare Driver. This would include when they are logged in to the Rideshare application waiting for a customer match, on their way to pick up a customer, but not when a customer has entered the vehicle.

When a driver is working as a Rideshare Driver, this new Rideshare coverage will protect them from the following types of risks, and there is a need to be able to collect the appropriate information about the losses:

. Injury to a first-party driver

. Damaged personal property of the third-party passengers

Which two exposures need to be configured? (Choose two.)

- A. Rideshare Liability Under Insured Motorist

- B. Rideshare Liability Personal Injury Protection

- C. Rideshare Medical Payments

- D. Rideshare Liability Bodily Injury

- E. Rideshare Personal Property Protection

Answer: C,E

Explanation:

250 to 350 words From Exact Extract of Guidewire ClaimCenter Business Analyst documentation:

To satisfy the requirements for the new "Rideshare" coverage product, the Business Analyst must map the described risks to the correct Exposure Types in the ClaimCenter data model.

* Risk: Injury to a first-party driver:In insurance terminology, "First Party" refers to the insured (the driver). Coverage for injuries sustained by the driver themselves is typically handled byMedical Payments(MedPay) or Personal Injury Protection (PIP). Among the choices provided,Rideshare Medical Payments (Option C)is the correct exposure type to cover medical costs for the driver regardless of fault. (Option E, Liability Bodily Injury, would cover injuries toothersthat the driver hit).

* Risk: Damaged personal property of third-party passengers:This refers to liability for damage to property belonging to others. While typically "Property Damage Liability," the specific option provided that fits this description isRideshare Personal Property Protection (Option B). This exposure would be configured to capture details about the damaged items (e.g., luggage, electronics) belonging to the passengers.

Why other options are incorrect:

* Option E (Liability Bodily Injury):This is for Third Party injuries (e.g., pedestrians or people in other cars), not the First Party driver.

* Option D (Under Insured Motorist):This applies when the Rideshare driver is hit by someone else who doesn't have enough insurance. The prompt focuses on the risksofthe driver working, not the financial failure of others.

NEW QUESTION # 33

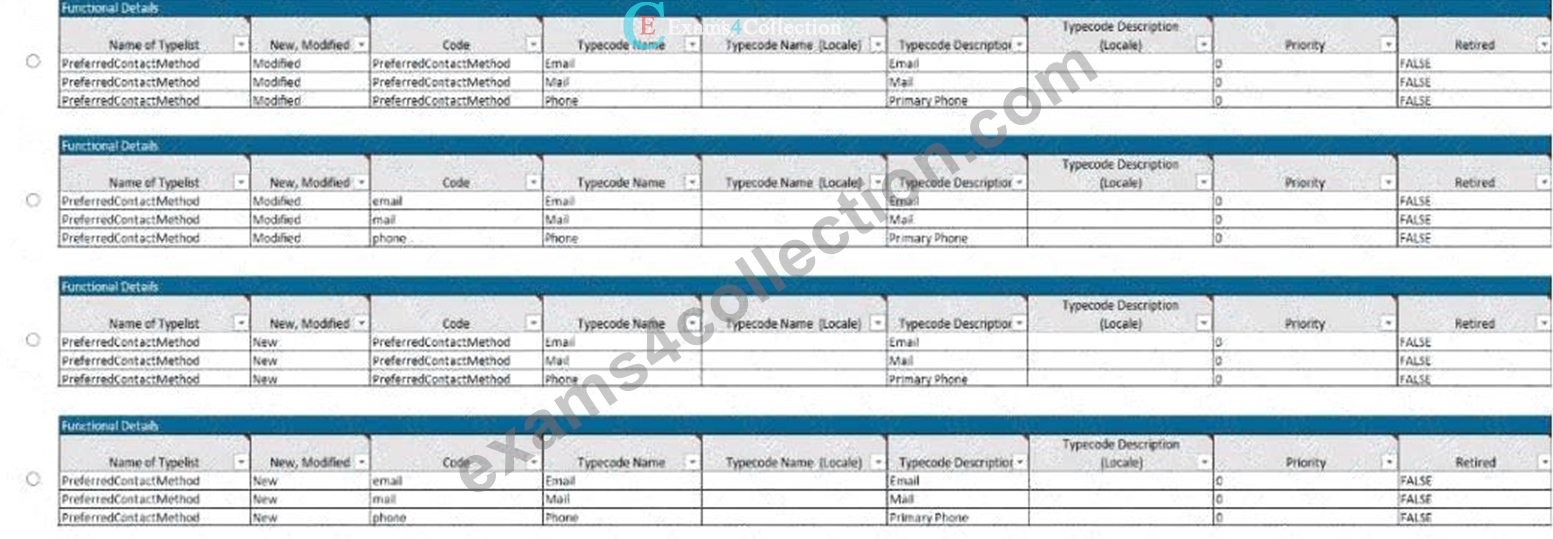

During claim intake and adjudication, Adjusters capture contact information for the insured and all claimants.

To improve customer service and reduce the time required to reach these contacts to gather additional claim information, Succeed Insurance will capture the preferred contact method for all person contacts. The new field will be added to the contact details screen of the user interface (UI) as a drop-down list displaying all valid contact methods including email, mail, and phone.

Which version correctly lists the preferred contact methods in the Typelists tab of the Parties Involved User Story Card?

- A. Option B

- B. Option A

- C. Option C

- D. Option D

Answer: A

Explanation:

To correctly document a Typelist in a User Story Card, the Business Analyst must understand both the data structure (Codes vs. Names) and the configuration state (New vs. Modified).

* Code Validity:In Guidewire, aTypecode(the value stored in the database) must be a unique identifier for each option in the list.

* Option Bcorrectly lists distinct codes: email, mail, and phone.

* Options A and Care incorrect because they list theTypelist Name(PreferredContactMethod) as the Codefor every single row. You cannot have multiple entries with the same primary key (Code) in one list.

* Configuration State (New vs. Modified):The PreferredContactMethod typelist is a standardBase Productfeature in Guidewire ClaimCenter. It already exists out-of-the-box.

* Option Bcorrectly identifies the Status as"Modified". When you add values to or configure an existing base typelist, you document it as "Modified".

* Option Dis incorrect because it lists the Status as"New". This would imply creating a brand new custom typelist (e.g., MyCustomList_Ext), which is not necessary for standard contact methods.

Therefore,Option Bis the only version that has valid, unique codes and the correct configuration status.

NEW QUESTION # 34

What is the importance of a mock-up of the user interface (UI) design?

- A. A mock-up illustrates for the customer what the final ClaimCenter user experience is.

- B. A mock-up shows the viewer what the intended ClaimCenter user experience is.

- C. A mock-up tells the customer what the current ClaimCenter user experience is.

- D. A mock-up illustrates for the viewer the integration of ClaimCenter with outside sources.

Answer: B

Explanation:

In the context of a Guidewire implementation project, a User Interface (UI) Mock-up is a visual tool used during the requirements gathering and design phases. Its primary purpose is to illustrate the intended user experience before development begins.

* Visualization of Requirements:Mock-ups bridge the gap between abstract written requirements (User Stories) and the concrete software product. They show stakeholders how the screens will look and function to meet their needs.

* Intended vs. Final:Option A is correct because the mock-up represents theproposedorintendeddesign.

Option D ("Final") is subtly incorrect because the "final" experience is the actual, functioning software, which may evolve slightly from the mock-up during development due to technical constraints or feedback.

* Current vs. Integration:Option B refers to the existing system (Current state), which is typically shown via live demo, not a mock-up. Option C refers to backend integrations, which are typically documented via data mapping spreadsheets or architecture diagrams, not UI mock-ups.

NEW QUESTION # 35

Succeed Insurance has plans to expand operations in Greeley, Colorado. Due to a history of hailstorm related damage in the area, the company plans to offer reimbursement for hail damage as an option.

Which two actions should the Business Analyst (BA) take to determine the requirements for the project?

(Choose two.)

- A. Author user stories following the elaboration workshops and identify acceptance criteria.

- B. Recommend existing base product features and functionality to expedite the implementation.

- C. Identify changes to the line of business typelists and determine the correct data mapping.

- D. Lead an elaboration workshop with the customer and follow up to identify next steps.

Answer: B,D

Explanation:

In the Guidewire delivery methodology, the "Determine Requirements" phase (often part of Inception or Elaboration) focuses on understanding the business need and mapping it to the software capabilities.

* Lead an Elaboration Workshop (A):TheElaboration Workshopis the primary forum where BAs engage with stakeholders (like the Greeley operations team) to discuss the specific needs for the new

"hail damage" product. This is where the raw requirements are gathered, discussed, and refined.

* Recommend Base Product Features (B):A critical responsibility of the Guidewire BA is to maximize product value by reducing unnecessary customization. When determining requirements for

"reimbursement" and "hail damage," the BA should immediately demonstrate and recommend how ClaimCenter's out-of-the-box Coverage, Exposure, and Incident features can handle this scenario. This aligns the customer's expectations with the standard software capabilities, expediting the implementation.

* Why not C or D?Authoring user stories (C) and defining typelists (D) areoutputsortasksthat occurafter the requirements have been determined and the solution approach (Standard vs. Custom) has been agreed upon.

NEW QUESTION # 36

Succeed Insurance is expanding into California, Texas, and Arizona which have large Spanish-speaking customer bases. Currently language is not considered in assignment. Succeed wants the ability to assign claims to appropriate bilingual Adjusters. Succeed also needs the ability to identify the preferred language of the customers.

The company is planning to implement a slightly modified version of ClaimCenter to suit its organization's needs. The modification will include adding two new required fields to the existing user interface (UI) to capture the reporter's Preferred Language and Preferred Contact Time. This requirement is critical for Succeed to enhance the operational efficiency and expediency of claims processing in its region.

Which two guiding principles apply to this implementation? (Choose two.)

- A. We are not building a system from scratch.

- B. We will not revisit decisions already documented.

- C. We will challenge current processes.

- D. We will include scope that accelerates time-to-market.

Answer: A,C

Explanation:

In Guidewire implementation projects (often following the SurePath methodology), specific Guiding Principles are established to manage scope and ensure project success.

* "We are not building a system from scratch" (Option A):This is the foundational principle of package software implementation. The scenario explicitly states that Succeed is implementing a

"slightly modified version of ClaimCenter" (using the base product) rather than building a custom solution. The project team accepts that they are starting with a robust, pre-built application and will only modify it where necessary (e.g., the two specific fields).

* "We will challenge current processes" (Option B):The scenario notes that "Currently language is not considered in assignment." To successfully implement the new requirement (bilingual assignment), the project team must challenge and change the legacy business process. Instead of automating the old way of working (which ignored language), they are defining a new, more efficient process that leverages the tool's capabilities.

Why other options are incorrect:

* Option C:Adding scope (new fields) generallyincreasesrisk and time rather than accelerating it, unless the scope is strictly MVP. The primary focus here is efficiency, not just speed of deployment.

* Option D:While "not revisiting decisions" is a good governance rule, it is not the primary principle illustrated by the decision to modify the UI for specific business value.

NEW QUESTION # 37

Which set of three objects is required to create a liability exposure?

- A. Claimant, Coverage (type and subtype), Reserve Line

- B. Coverage (type and subtype), Incident, Reserve Line

- C. Claimant, Coverage (type and subtype), Incident

- D. Claimant, Incident, Reserve Line

Answer: C

Explanation:

In the Guidewire ClaimCenter object model, a Liability Exposure represents a specific potential financial obligation to a third party. To successfully instantiate (create) a new exposure record, the system requires three fundamental data associations to define "Who, What, and How":

* Claimant:The specific person or entity seeking compensation (the "Who"). Every exposure must be linked to a contact designated as the claimant.

* Coverage (Type and Subtype):The specific contractual provision from the policy that applies to the loss (the "How"). The exposure must link back to a valid coverage on the verified policy to confirm the insurer is liable.

* Incident:The specific details of the event or damage (the "What"). In ClaimCenter, anIncidentis a distinct object (e.g., Vehicle Incident, Injury Incident) that captures the facts of the loss. Multiple exposures can link to the same incident (e.g., Bodily Injury and Property Damage exposures both linking to the same Vehicle Incident), but every exposure requires one underlying incident to define the scope of the damage.

Why other options are incorrect:

* Reserve Line (A, C, D):A Reserve Line is a financial accounting object createdafterthe exposure exists to set aside funds. It is a child object of the exposure, not a prerequisite for creating the exposure itself.

NEW QUESTION # 38

To optimize business process workflow, an insurer has spent a great deal of effort on estimating the amount of effort required to complete various types of work... They are also aware that certain situations may require specialized expertise and want to incorporate this in their decision making.

All claims and exposures are entered using only the ClaimCenter new claim wizard. Once entered, the work should be automatically distributed fairly to those properly suited, as determined by the company's knowledge of each worker's skill set.

Which two assignment mechanisms, alone or together, will achieve their goal? (Choose two.)

- A. Round-robin

- B. User attribute

- C. Supervisor assignment

- D. FNOL queues

- E. Weighted workload

Answer: B,E

Explanation:

To meet the dual requirements of "specialized expertise" and "fair distribution based on effort," the Business Analyst should utilize User Attributes and Weighted Workload assignment rules.

* User Attributes (Option B):This feature handles the "specialized expertise" requirement.

Administrators can tag users with specific attributes (e.g., "Bilingual," "Heavy Equipment Expert,"

"Litigation Specialist"). Assignment rules can then be configured to filter the pool of potential assignees toonlythose who possess the matching attribute for the specific claim type.

* Weighted Workload (Option D):This feature handles the "fair distribution" and "amount of effort" requirement. Unlike Round-robin (which treats all claims as equal), Weighted Workload assigns a

"weight" (effort points) to the claim and tracks the "load factor" (current capacity) of the user. The system assigns the new work to the user with the lowest relative workload, ensuring that adjusters handling difficult, high-effort claims are not overwhelmed with the same volume as those handling simple claims.

Why other options are incorrect:

* Round-robin (A):Distributes work purely cyclically (1-2-3-1-2-3) without regard for the user's current workload or the complexity of the claim.

* FNOL Queues (C):This is a "pull" mechanism where work sits in a bucket until someone grabs it, rather than the "automatic distribution" (push) requested.

* Supervisor Assignment (E):This is manual, not automatic.

NEW QUESTION # 39

What is a reason to assign a unique identification number to each User Story Card in ClaimCenter implementation projects?

- A. The number is used in the naming convention of: Product - Theme - Subtheme - ID number.

- B. The number helps to identify accepted and rejected Acceptance Criteria on Burndown Charts.

- C. The number provides the primary means for organizing tasks in backlog.

- D. The number identifies total time estimated for building out the related User Story.

Answer: A

Explanation:

In Guidewire implementation methodology (such as SurePath), traceability and organization are maintained through strict naming conventions.

* Naming Convention (Option C):A unique identification number is assigned to every User Story Card to create a consistent naming structure:Product - Theme - Subtheme - ID. (For example: CC - FNOL - Vehicle - 001).

* Purpose:This convention allows Business Analysts, Developers, and QA testers to easily reference, search, and trace requirements across different tools (e.g., from the Story Card in Excel/Jira to the code in Studio and the test cases in the testing suite).

* Why not A, B, or D?Time estimation (A) uses "Story Points," not the ID. Burndown charts (B) track velocity/points, not criteria IDs. Backlogs (D) are organized byBusiness Value/Priority, not just numerically by ID.

NEW QUESTION # 40

Succeed Insurance has a requirement to add a new high-risk indicator to the Claim Status screen for property claims that have a lien on the property. A new icon will be added to the configuration to provide a visual indicator making it easier for Adjusters and other ClaimCenter users to determine that a claim has a lien.

Which two common areas of the user interface (UI) can display the new lien icon? (Choose two.)

- A. Screen Area

- B. Tab Bar

- C. Sidebar

- D. Info Bar

- E. Workspace

Answer: A,D

Explanation:

In the standard Guidewire ClaimCenter User Interface architecture, high-priority alerts and claim indicators are displayed in two primary locations to ensure visibility:

* The Info Bar (Option D):This is the persistent strip located at the top of the claim file (just below the Tab Bar). It remains visible regardless of which specific claim sub-screen (Medical, Financials, Notes) the user is navigating. It is designed specifically to host "High Risk Indicators" such as Litigation, Fatalities, Coverage issues, and in this scenario, a "Lien" indicator. This ensures the adjuster is aware of the critical status immediately upon opening the claim.

* The Screen Area (Option A):Specifically, theClaim Status(or Summary) screen-which resides in the main Screen Area-contains a dedicated section for "Claim Indicators." Here, the icon is displayed along with a text description and potential toggle status (On/Off). The prompt explicitly mentions the requirement to "add a new high-risk indicator to the Claim Status screen," confirming the Screen Area as the second location.

Why other options are incorrect:

* Sidebar (B):The sidebar (left panel) is used for the "Actions" menu and navigation links (steps) to move between screens. It does not typically host status icons for the claim object itself.

* Workspace (C):While "Workspace" can refer to the application frame, in UI terminology, it often refers to the specific worksheets (bottom pane) or the container, not the specific UI element for indicators.

* Tab Bar (E):The Tab Bar is for high-level navigation (Claim, Desktop, Administration, Search) and does not display claim-specific data icons.

NEW QUESTION # 41

Losses incurred because of an accident with other vehicles can be very large. Because of the risk of large losses, all claims must include both a police report and the details of any passengers in the vehicle, whether they sustained injuries or not. The claim must show whether there were passengers in the vehicle at the time of the accident. Succeed wants the ability to include a very detailed description of the loss event information on intake of the claim.

When the claim is created, Succeed wants to flag the claim with a reminder for the Adjuster to contact the insured.

There should be reminders for the Adjuster to complete the following items for every new claim created:

. Review any photographs of the accident

. Contact and Interview each passenger

. Collect statements from each witness

. Record the vehicle's mileage

Which business requirement is based on assumptions?

- A. When the claim is created, we want to flag the claim with a reminder for the Adjuster to contact the insured.

- B. All claims must include both a police report and the details of any passengers in the vehicle, whether they sustained injuries or not.

- C. There should be reminders for the Adjuster to complete the following items for every new claim created: review any photographs of the accident.

- D. There should be reminders for the Adjuster to complete the following items for every new claim created: collect statements from each witness.

Answer: C

Explanation:

In the context of business requirements analysis, an assumption is a statement that is accepted as true or certain to happen without proof.

* Why A is the correct answer:The requirement to generate a reminder to "review any photographs" for everynew claim assumes that photographs will be available for every accident. In reality, photos are not always taken or provided at the First Notice of Loss (FNOL). Creating a mandatory task for an optional piece of evidence is based on the assumption of data availability.

* Why D is incorrect:"All claims must include a police report..." is aBusiness Ruleor constraint. It is a mandatory condition imposed by the business ("must include") rather than an assumption about what is currently present.

* Why B is incorrect:Contacting the insured is a standard, universal step in the claims process that applies to every claim, so it is not considered an assumption.

NEW QUESTION # 42

Succeed Insurance has a strategic initiative to offer pay-as-you-drive personal auto insurance to compete with other large carriers. Customers who choose these policies must either own a vehicle that is equipped with a monitoring device or agree to install a device provided by Succeed. The monitoring device collects information about how the drivers of a covered vehicle drive, including how fast they drive, how hard they brake, and how many miles/kilometers the vehicle travels within a policy period.

This information is logged, and premiums are based on how the insured's driving behavior is categorized.

When a claim is reported, the log files must be obtained to analyze the information captured by the monitoring device at the time of the incident.

Succeed plans to collect and evaluate the Vehicle Monitoring Log files in the first implementation phase, which is scheduled for release in 60 days. The project sponsors have instructed the implementation team to use base product functionality over customization. Integration should be leveraged where possible to avoid manual data entry.

No payments can be made on the claim until a flag indicating that the Vehicle Monitoring Log file has been processed has been set to 'Yes'.

Which feature of the base product prevents payments from being made on the claim?

- A. Transaction Validation rule requiring approval for payments with unprocessed log files.

- B. Validation rule enforcing the Ability to pay validation level.

- C. Authority Limit for any payment with a policy type of Pay-as-you-drive.

- D. Validation rule enforcing the Send to external system validation level.

Answer: B

Explanation:

In Guidewire ClaimCenter, the Ability to Pay validation level is the specific "gatekeeper" designed to verify that a claim is mature enough and has sufficient data to allow financial transactions to be issued.

* Validation Levels:ClaimCenter uses validation levels (e.g., Load, New Loss, Ability to Pay) to enforce data integrity at different stages of the claim lifecycle.

* Blocking Payments:When a user attempts to create a check, the system triggers the rules associated with theAbility to Paylevel. If any rule at this level fails (returns an error), the system prevents the payment wizard from completing.

* Scenario Application:The Business Analyst can define a rule at the "Ability to Pay" level that checks the condition:"If Policy Type is Pay-as-you-drive AND Log Processed Flag is NOT 'Yes', then throw an error."This fulfills the requirement to strictly block payments ("No payments can be made") rather than just route them for approval.

Why other options are incorrect:

* Authority Limits (B)control theamountof money a user can approve, not the prerequisites (like data flags) for making a payment.

* Transaction Validation requiring approval (C)would route the payment to a supervisor, but it implies the paymentcouldbe made if approved. The requirement states "No payments can be made," implying a hard system stop, which validation rules provide.

* Send to External System (D)validates data just before it leaves the system (e.g., for check printing), which is often too late in the workflow for business-logic stops like reviewing a log file.

NEW QUESTION # 43

Succeed Insurance has a strategic initiative to offer pay-as-you-drive personal auto insurance to compete with other large carriers. Customers who choose these policies must either own a vehicle that is equipped with a monitoring device or agree to install a device provided by Succeed. The monitoring device collects information about how the drivers of a covered vehicle drive, including how fast they drive, how hard they brake, and how many miles/kilometers the vehicle travels within a policy period.

This information is logged, and premiums are based on how the insured's driving behavior is categorized.

When a claim is reported, the log files must be obtained in order to

analyze the information captured by the monitoring device at the time of the incident.

Succeed plans to collect and evaluate the Vehicle Monitoring Log files in the first implementation phase, which is scheduled for release in 60 days. The project sponsors have instructed the implementation team to use base product functionality over customization. Integration should be leveraged where possible to avoid manual data entry.

The New Claim Wizard must capture whether or not the vehicle has a monitoring device installed when a personal auto claim is created against a pay-as-you-drive policy.

Which feature of the base product enforces this claim creation requirement?

- A. Create a Validation rule enforcing the Ability to pay validation level.

- B. Create a Validation rule enforcing the New loss completion validation level.

- C. Create a Validation rule enforcing the Load and save validation level.

- D. Create a Validation rule enforcing a new custom Validation level for mechanical requirements.

Answer: B

Explanation:

In Guidewire ClaimCenter, Validation Rules are used to enforce data integrity and business requirements at specific stages of the claim lifecycle. These stages are defined by Validation Levels.

* New Loss Completion (Option B):This validation level is specifically designed as the "gatekeeper" for the New Claim Wizard (FNOL). Rules triggered at this level run when the user attempts to click

"Finish" to submit the new claim. If a rule fails (e.g., "If Policy Type = Pay-as-you-drive AND Monitoring Device is Null"), the system prevents the claim from being created and highlights the missing field. This directly meets the requirement to enforce data capture "when a personal auto claim is created." Why other options are incorrect:

* Ability to Pay (A):This level runs when a user tries to issue a check. Using this would allow the claim to be createdwithoutthe device info, only blocking the user later when they try to pay, which is too late for the requirement.

* Custom Level (C):Creating custom levels is possible but discouraged when a standard level fits the purpose, aligning with the "use base product functionality" principle.

* Load and Save (D):This level runs every time the claim is saved (even as a draft). Enforcing mandatory fields here can frustrate users who need to save their work partially complete.

NEW QUESTION # 44

What are two recommended best practices with user interface (UI) mock-ups in a ClaimCenter implementation project? (Choose two.)

- A. A live system demonstration is acceptable in place of using a user interface (UI) mock-up to describe needed changes to the user interface.

- B. When creating a user interface (UI) mock-up, a Business Analyst (BA) should take a clear screen shot.

User interface (UI) mock-up tools should not be used. - C. When a Business Analyst (BA) does not have access to a tool, it is acceptable to take a clear screen shot, then indicate on the image how the screen should appear to meet the requirements.

- D. A Business Analyst (BA) should document the requirement number associated with the mock-up and then use a user interface (UI) mock-up tool to build the mock-up.

Answer: C,D

Explanation:

In a Guidewire implementation, User Interface (UI) mock-ups serve as critical visual aids to bridge the gap between written business requirements and the final technical solution.

* Best Practice 1 (Option B):While sophisticated prototyping tools (like Balsamiq or Axure) are valuable, they are not always strictly necessary for every change. A "low-fidelity" mock-up is often sufficient and highly effective for minor adjustments. If a BA lacks access to specialized software, the recommended best practice is to take a screenshot of the existing ClaimCenter screen and overlay it with text boxes, arrows, or simple graphics (using tools like Paint or PowerPoint) to clearly indicate where fields should be added, moved, or removed. The goal is clarity of intent, not artistic perfection.

* Best Practice 2 (Option D):Traceability is fundamental to the Agile and hybrid methodologies used in Guidewire projects. Every artifact, including mock-ups, must be traceable back to the specificUser StoryorRequirement Numberit supports. By explicitly documenting the requirement number on or with the mock-up, the BA ensures that developers understand exactly which functionality is being visualized and that QA testers can validate the final screen against the correct scope.

Why other options are incorrect:

* Option A:A live demo shows thecurrentstate. It cannot effectively demonstratefuturechanges (fields that don't exist yet) without a visual mock-up to accompany the explanation.

* Option C:Stating that tools "should not be used" is incorrect; tools are generally encouraged when available to create high-fidelity prototypes.

NEW QUESTION # 45

Which two components are necessary to create the check(s) using the wizard? (Choose two.)

- A. Payment tied to a reserve line

- B. Date of the claim

- C. Payment tied to an activity

- D. Payee

Answer: A,D

Explanation:

The Check Wizard in Guidewire ClaimCenter enforces strict financial integrity rules. To successfully create a check, the user must define the source of funds and the recipient.

* Payment tied to a Reserve Line (Option A):Every payment must be allocated to a specificReserve Line(combination of Exposure, Cost Type, and Cost Category). This ensures that the payment consumes the correct financial reserves and maps to the correct coverage on the policy. You cannot create a "floating" payment; it must be tied to a reserve line.

* Payee (Option C):A check is a legal instrument that must be payable to a specific entity. Selecting a Payee(from the claim contacts) is a mandatory step in the wizard.

Why other options are incorrect:

* B (Activity):While paymentscanbe linked to activities (e.g., Service Requests), it is optional. Most indemnity payments are made directly without an underlying activity.

* D (Date of claim):The Loss Date is a property of the claim, but it is not a component selected or created duringthe check wizard process. The relevant dates in the wizard are the "Service Period" or

"Scheduled Send Date."

NEW QUESTION # 46

......

Ultimate Guide to Prepare Free ClaimCenter-Business-Analysts Exam Questions and Answer: https://drive.google.com/open?id=1aaG4tVi93cEh11DkN56sLi5x1LT3IsXh

Pass ClaimCenter-Business-Analysts Tests Engine pdf - All Free Dumps: https://www.exams4collection.com/ClaimCenter-Business-Analysts-latest-braindumps.html